CAM Reconciliation: A Step-by-Step Guide for Mid-Size Commercial Property Management Firms

Quick Summary: CAM reconciliation is the year-end process of comparing the estimated CAM charges tenants paid each month against your property's actual operating costs, then billing or crediting the difference. For mid-size commercial property management firms, doing it accurately protects net operating income, keeps tenant relationships clean, and turns the Q4 rush into a routine. This guide walks through the full eight-step CAM reconciliation process, the most common errors and how to catch them early, and the signs your workflow needs outside help.

Every fall, the same scene plays out inside mid-size property management firms across the country. Spreadsheets open across three monitors, a tenant emails to dispute their share of the parking lot repaving, and the property management system shows one expense total while the general ledger shows another. And the one person who really understood last year's numbers left in March.

If that sounds familiar, you are not behind because your team is weak. You are behind because common area maintenance (CAM) reconciliation is one of the hardest jobs in commercial property accounting, and most firms only treat it as a job once a year.

Get it wrong, or even just late, and you either absorb costs you were entitled to recover or hand a tenant a reason to challenge the bill. This guide walks through how CAM reconciliation actually works, step by step, for commercial property management firms managing 500 to 2,500 tenants, where the stakes and the complexity are both real. You will get the full process, the mistakes that cause tenant disputes, and a clear way to tell whether your current workflow can scale with your portfolio.

Let's start with a clear definition, because a lot of CAM trouble begins with a fuzzy one.

What Is CAM Reconciliation?

CAM reconciliation is the process of comparing the estimated common area maintenance charges you billed tenants during the year against the actual operating costs you incurred. If actual costs came in higher than the estimate, tenants owe the difference. If costs came in lower, tenants get a credit. The goal is a fair, lease-accurate true-up that holds up if a tenant challenges it.

Common area maintenance covers the shared costs of running a commercial property such as a retail center, office building, or mixed-use space: things like property taxes, insurance, landscaping, snow removal, parking lot upkeep, security, and utilities for common spaces. Tenants agree in their lease to cover a portion of these costs based on the space they occupy. Industry bodies such as the Building Owners and Managers Association (BOMA) publish widely used standards for how these operating costs are measured and classified.

Sounds simple. The hard part is that no two leases treat CAM the same way, and that variability is where the money quietly leaks out.

Why Mid-Size Firms Lose Money on CAM Reconciliation

For a small operator with a handful of tenants, a CAM error is an annoyance. For a mid-size firm with multiple properties, mixed tenant types, and dozens of leases, a CAM error becomes a pattern. And patterns get expensive.

Here is what poor CAM reconciliation actually costs you. Under-billing means you absorb operating costs you had every right to recover, which quietly drains net operating income (NOI) across the portfolio. Over-billing or sloppy math invites disputes, and a tenant dispute is rarely just a phone call. It can trigger a formal audit request, strain a relationship you spent years building, and in the worst cases create legal exposure.

There is also a trust cost. When statements go out late or look inconsistent, sophisticated tenants notice. So do the owners and investors who expect you to run a clean operation. CAM accuracy is one of the clearest signals that your back office is in control, which is why, as portfolios grow, many firms start weighing the broader benefits of outsourcing accounting against stretching a lean team even further.

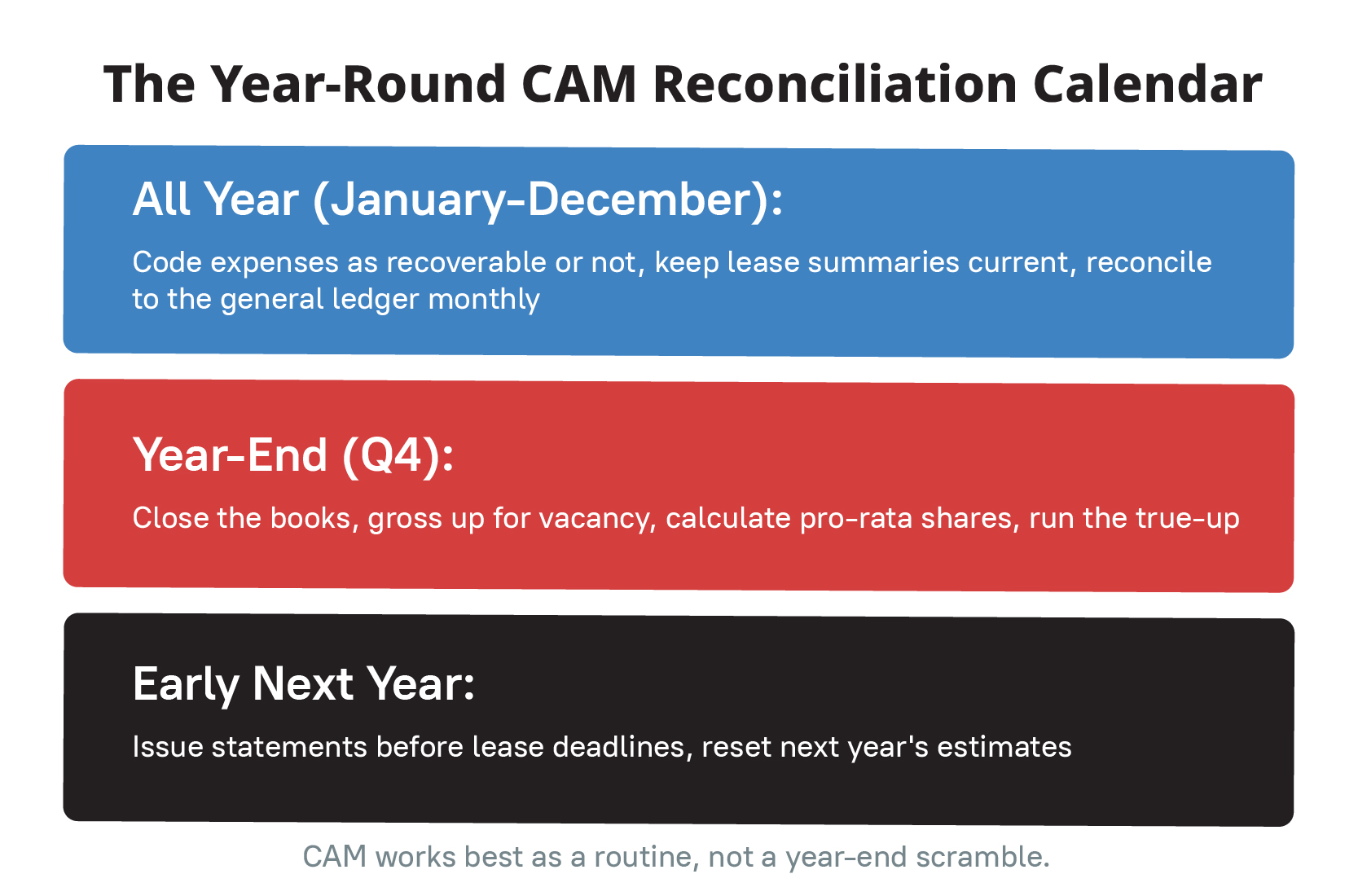

The firms that handle CAM well share one habit: they treat it as a year-round process, not a Q4 fire drill. That single shift is the difference between a clean close and a mad dash.

To see why that year-round habit matters so much, look at the two stages CAM actually runs on.

Monthly Billing vs. Year-End True-Up: The Two-Stage Process

Before the steps, it helps to see CAM as two connected stages, because confusing them is where a lot of firms slip.

Stage one runs all year. Each month, tenants pay an estimated CAM charge alongside base rent. You base that estimate on projected operating costs, and it lands on the tenant ledger every billing cycle. This is the cash flowing in throughout the lease year.

Stage two happens once, at year-end. You add up what each tenant actually owed based on real costs, then compare it to what they already paid in monthly estimates. The gap between the two is the true-up. Tenants who underpaid get a bill. Tenants who overpaid get a credit.

The mistake is treating stage one as "done" and only thinking about CAM at stage two. The monthly estimates and the year-end true-up are the same process at two points in time. When the monthly side is sloppy, the year-end side becomes a reconstruction project instead of a reconciliation.

Here is how to run both stages cleanly, one step at a time.

The CAM Reconciliation Process: 8 Steps From Estimates to True-Up

Here is the full process a mid-size firm should follow. Steps 1 through 3 run throughout the year, and steps 4 through 8 happen at year-end. The logic is the same whether you run AppFolio, Yardi, MRI, or Buildium. What changes is where each step lives in your system, and a few platform notes are called out below.

Step 1: Set the Estimated Monthly CAM Charges

At the start of the lease year, you estimate each tenant's monthly CAM payment based on projected operating costs, usually built from the prior year's actuals plus expected increases. Tenants pay this estimate every month along with base rent. Getting the estimate close matters. A wildly low estimate sets up a painful true-up bill later, and an inflated one creates friction all year.

Step 2: Track and Categorize Expenses as You Go

Throughout the year, record every qualifying operating expense as it hits: taxes, insurance, repairs, utilities, landscaping, security. Two habits save you in December. First, tag each cost as recoverable or non-recoverable right away, because capital improvements and single-tenant charges do not belong in the shared pool. Second, split the recoverable costs into fixed, like management fees, and variable, like daily cleaning or snow removal. Only the variable bucket gets grossed up later, so separating it now matters. Firms that skip this lose days untangling it at year-end.

Step 3: Apply Lease-Specific Inclusions, Exclusions, and Caps

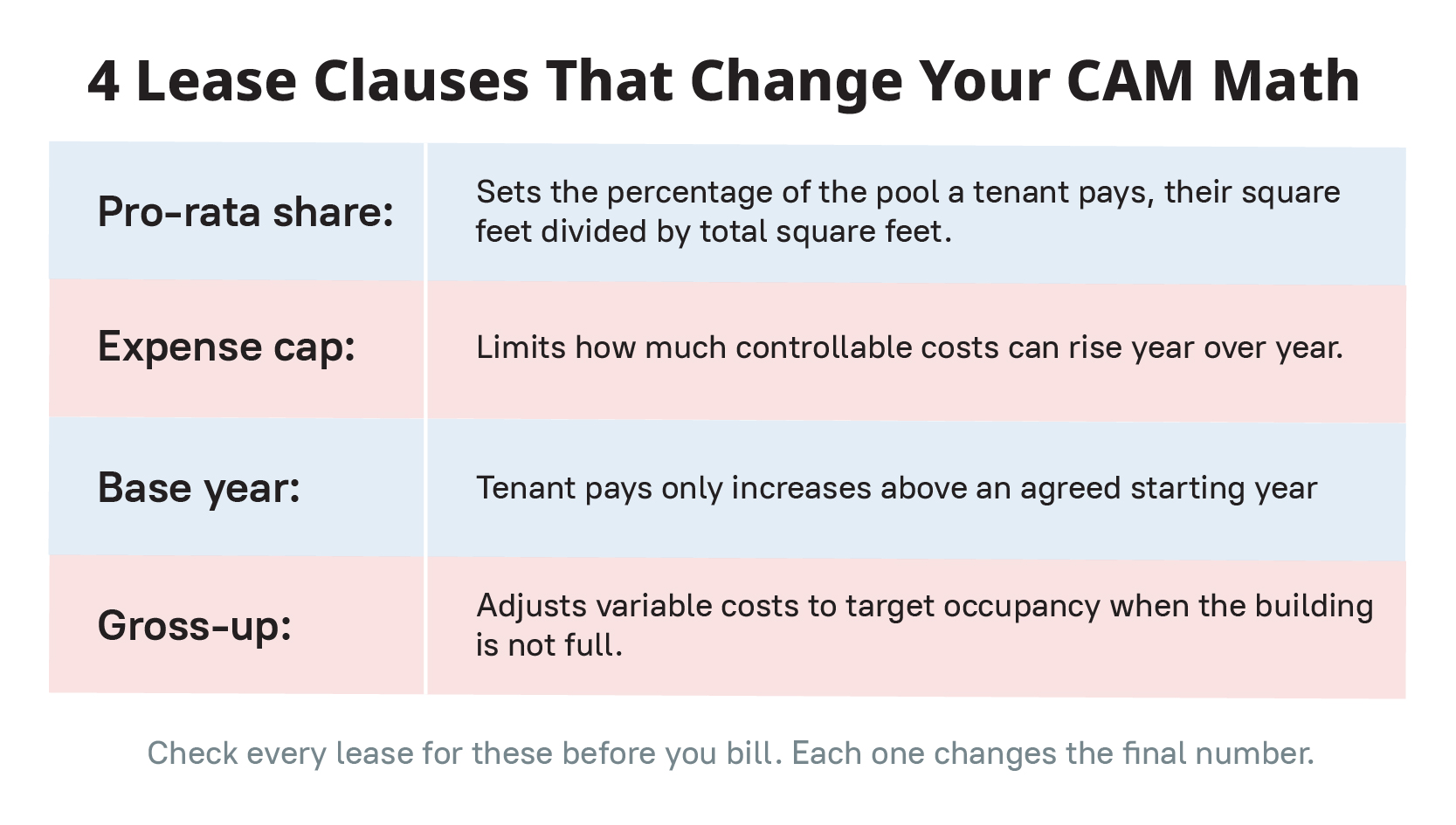

This is where CAM gets technical. Each lease dictates which expense categories apply to that tenant, whether there are caps on annual increases, whether a base year applies, and how the pro-rata share is calculated. One tenant's lease might exclude management fees. Another might cap controllable expenses, the costs you can manage like landscaping and cleaning, at 5% growth a year, while leaving non-controllable costs like property taxes and insurance uncapped. A third might use a different square-footage denominator entirely. You have to read and apply each lease on its own terms. Working from lease summaries kept current through the year, sometimes called lease abstractions, makes this far faster.

Step 4: Close the Books and Tie the System to the General Ledger

At year-end, close the books before you reconcile anything. Wait for late vendor invoices, especially those December bills, to post or get accrued, so no real cost goes missing from the pool. Then confirm that your property management platform and your general ledger actually agree. In mid-size firms running AppFolio, Yardi, MRI, or Buildium, the subledger and the general ledger tend to drift apart over twelve months. A statement built on numbers that do not tie will not survive a tenant audit. Reconcile first, bill second.

Step 5: Apply Gross-Up Adjustments for Vacancy

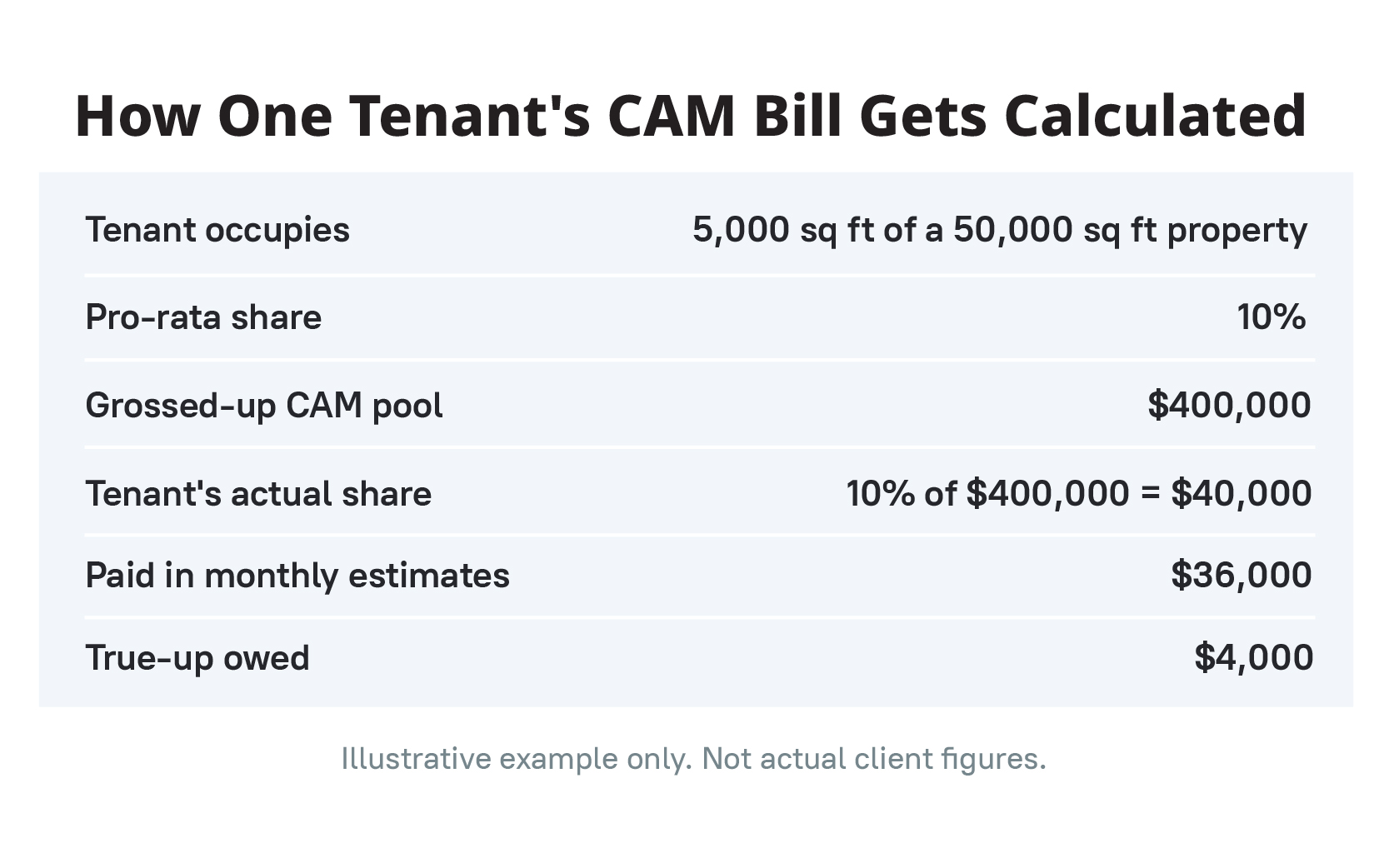

If the property was not fully occupied all year, you gross up the variable expenses. The reason is simple: costs like cleaning and utilities rise and fall with occupancy, so billing only the actual costs of a half-empty building would shortchange your recovery and unfairly load the few tenants who were there. The fix is a gross-up factor. You divide the lease's target occupancy, often 95%, by the actual average occupancy, then multiply the variable expenses by that factor. Apply it only to variable costs, and only where the lease allows it. This one trips up a lot of teams, and getting it wrong is a common reason tenants push back.

Step 6: Calculate Each Tenant's Pro-Rata Share

Now you work out how much of the grossed-up pool each tenant owes. Most allocations run on a pro-rata basis, meaning a tenant's share equals their square footage divided by the property's total leasable area:

Pro-rata share = Tenant's rentable square feet ÷ Total rentable square feet

So a tenant in 5,000 square feet of a 50,000 square foot property has a 10% pro-rata share. Multiply that percentage by the eligible, grossed-up CAM expenses to get their liability for the year, which means a $400,000 pool leaves that tenant owing $40,000. Watch your pools while you do this. Some properties run multiple pools, like one for the whole center and one for a specific building. Allocate to the wrong pool and every downstream number is off. AppFolio handles this through its CAM and recovery setup, while Yardi runs it through recovery groups, so the setup screen differs but the logic does not.

Step 7: Reconcile Estimated Against Actual: The True-Up

Now compare what each tenant paid in estimates against their actual share of the real costs. This is the true-up. If a tenant paid $36,000 in estimates but their actual share came to $40,000, they owe $4,000. If they overpaid, they receive a credit. Tie every figure back to source documents, because this is the number a tenant is most likely to question.

Step 8: Issue Audit-Ready Statements and Reset Next Year's Estimates

Produce a clear reconciliation statement for each tenant, with supporting detail, and send it before your lease deadlines. Include the expense breakdown, the tenant's pro-rata share, what they paid, and the resulting balance or credit, and keep the underlying invoices on hand for audit-conscious tenants.

Clean documentation here is your best defense against disputes, because most disputes come from statements tenants cannot follow, not from honest math errors. Then close the loop. Use this year's actuals to reset next year's monthly estimates, which shrinks the true-up and the surprises that come with it.

Run these eight steps in order and the year-end true-up stops being a scramble. One related term still causes confusion, though, and it is worth clearing up next: how a CAM audit differs from the reconciliation itself.

CAM Audit vs. CAM Year-End Reconciliation: What Is the Difference?

People use these terms loosely, so it helps to separate them.

A CAM year-end reconciliation is the true-up itself: the year-end process of comparing estimates to actuals and billing the difference, as laid out in the steps above.

A CAM audit is the review that confirms the reconciliation is right before it goes out, or the formal review a tenant requests after the fact under the audit rights in their lease. Those audit rights, and the practice norms around them, are shaped in part by professional property management standards from groups like the Institute of Real Estate Management (IREM). A proactive internal CAM audit, run before statements are issued, catches misallocated expenses, lease-term errors, and pool mistakes while you can still fix them quietly. The alternative is finding those errors after a tenant's accountant does.

Smart firms build the audit into the workflow. They do not wait for a tenant to request one.

Build that review in early and you head off the mistakes behind most disputes, which tend to be the same few every year.

The 5 Most Common CAM Errors: What They Cost and How to Catch Them Early

Most CAM problems trace back to a short list of avoidable errors. Here is what each one costs and the simplest way to catch it before it reaches a tenant.

Each of these is a process problem, not a talent problem. The fix is a consistent, documented workflow that runs all year.

The catch is that holding a workflow like that together gets harder as your portfolio grows, and at some point doing it all in-house starts to strain.

When DIY CAM Breaks Down: Signs You Need a Specialist Process

You do not need a heavy process for a single small property. You almost certainly do once CAM becomes a meaningful slice of recoverable income across several properties, which is exactly where mid-size firms live.

Watch for these signals. Your month-end close already stretches past 15 days, so there is no spare capacity for CAM when Q4 hits. You lost an accountant who held the CAM knowledge in their head, and it walked out the door with them. Tenant disputes are becoming routine instead of rare. Or you are adding properties and new markets faster than your back office can absorb them. Any one of these means your current CAM approach has reached its ceiling. They are also some of the clearest signs it is time to hire a real estate accountant.

The goal is steady-state CAM: expenses coded correctly as they hit, lease terms kept current, pools reviewed on a rolling basis, and a clean internal review before billing. Some firms get there by tightening their own workflow and documenting it so it no longer lives in one person's head. Others bring in a specialist CAM reconciliation process run by a team who already know the work and the platforms, so there is no ramp-up. Either path beats the annual rush. The point is to choose a process on purpose rather than rediscovering the problem every December.

Whichever route fits your firm, a few habits keep CAM from running the show.

Actionable Takeaways

- Treat CAM as a rolling, year-round process. Code expenses correctly as they happen, not in a December rush.

- Keep lease summaries current. Every amendment should update how that tenant's CAM is calculated.

- Run an internal review before billing. Catch pool and cap errors while you can still fix them quietly.

- Reconcile your property management system to the general ledger before any statement goes out.

- Make tenant statements clear and well documented. Most disputes come from confusing statements, not bad math.

None of this takes heroics. It takes a system you run on purpose.

Where Stronger CAM Reconciliation Starts: Getting It Off Your December To-Do List

CAM reconciliation rewards firms that treat it as a discipline, not a deadline. Get the monthly estimates close, code expenses cleanly all year, apply each lease on its own terms, reconcile to the general ledger, and review before you bill. The math is rarely the hard part. The process around it is, and that is the part you can actually fix.

If CAM is the piece that keeps your year-end on edge, building a steady, year-round process is usually where the relief starts. Some firms get there by tightening and documenting their own workflow. Others hand it to a dedicated real estate accounting team that already runs CAM inside AppFolio and Yardi. Either way, the goal is the same: make next December a wrap-up instead of a mad rush.

Frequently Asked Questions

How does CAM reconciliation work?

CAM reconciliation compares the estimated common area maintenance charges billed to tenants during the year against actual operating costs. If actual costs are higher than the estimate, tenants owe the difference. If costs are lower, tenants receive a credit. Each lease sets its own inclusions, exclusions, caps, and pro-rata method, so the calculation is done lease by lease.

What is the difference between a CAM audit and a CAM year-end reconciliation?

A CAM year-end reconciliation is the true-up itself, where you compare estimated charges to actual costs and bill the difference. A CAM audit is the review that verifies the reconciliation is accurate, either run internally before statements go out or requested by a tenant under their lease. The reconciliation produces the numbers; the audit confirms they are right.

How do mid-size property management firms usually handle CAM reconciliation?

Many handle it once a year under deadline pressure, which is where errors and disputes come from. The firms that handle it well treat CAM as a year-round process: coding expenses correctly throughout the year, keeping lease terms current, and running an internal audit before billing. As portfolios grow, some firms move CAM to a specialized outsourced team rather than carry a full-time specialist.

What expenses are typically included in CAM charges?

Common area maintenance usually covers shared operating costs such as property taxes, insurance, landscaping, snow and trash removal, parking lot upkeep, security, and utilities for common areas. Capital improvements and costs tied to a single tenant are generally excluded, though every lease defines its own inclusions and exclusions.

What is a gross-up in CAM reconciliation?

A gross-up adjusts variable operating costs to a target occupancy level, usually around 95%, when a property is not fully leased. Because costs like cleaning and utilities rise with occupancy, grossing them up lets the landlord recover the true cost of running shared spaces instead of underbilling because space sat empty. Gross-ups apply only to variable expenses and only where the lease allows them.

What are controllable and non-controllable CAM expenses?

Controllable expenses are costs a property manager can influence, like landscaping, cleaning, and security. Non-controllable expenses are largely fixed and outside your control, like property taxes, insurance, and utilities. The distinction matters because leases often cap how much controllable expenses can rise each year while leaving non-controllable costs uncapped.

What is a base year in CAM reconciliation?

In a base-year lease, the tenant pays only for CAM increases above an agreed starting year, called the base year. If base-year CAM came to $8 per square foot and this year's costs reach $9, the tenant covers their share of the $1 difference, not the full amount. It is common in office leases, so confirm whether a lease uses one before you bill.

How do you calculate a tenant's CAM pro-rata share?

Divide the tenant's rentable square footage by the property's total rentable square footage. A tenant in 5,000 square feet of a 50,000 square foot building has a 10% pro-rata share. You then multiply that percentage by the eligible, grossed-up CAM expenses to find the tenant's share for the year.

.svg)

.svg)